Do you have an investment strategy, or are you gambling?

Recently, somebody asked for my opinion of a certain stock they were considering buying. I never know quite how to answer that question because buying individual stocks isn’t part of the investment strategies we run. For 1, I’m not a big fan of owning individual stocks because I’d much rather own a commission-free, low-cost ETF that consists of 1,000 companies instead of buying only 1 company. And 2, it probably doesn’t matter so much as “what stock to buy” as much as it does to be able to answer “when should I buy it” and “when should I sell it.”

The reason this question irks me so much though, is because it gets at the root of most investors problem: they’re gambling, not investing. How do you know if you’re a gambler or an investor? The ex-airline pilot in me has created a checklist to find out. If you answer “no” to any of the questions, you’re probably just gambling with your money. Or even worse, if you use the services of an investment advisor and they answer “no” to any of the questions, you’re paying someone else to gamble with your money…not cool dude!

First, the nuts and bolts of what makes it an actual strategy:

- My investing decisions can be boiled down to rules that could be programmed into a computer and answer the following:

- what to buy

- when to buy it

- how much to buy

- what to sell

- when to sell it

- how much to sell

Now you see why asking me “what do you think of this stock” just seems odd to me. If it fits your investment strategy’s rules, buy the stock; if not, don’t buy it. It’s pretty linear thinking at this level. The idea of some stock jockey sitting in front of 15 computer screens watching their indicators with beads of sweat dripping down their forehead is Hollywood my friend, not Wall Street. Investing, pragmatic investing, is pretty damn boring. You run your system, you follow the rules, you go on about your day. Once the rules are developed, it’s all about the proper execution of the strategy and just following the rules. Think about weight loss for example. You eat healthy, eat less, you exercise. You just follow the steps and the results will happen. That’s why it’s so important to focus on “process”, not “outcome.” You can’t change the outcome. That just happens. But we can change our process. And a better process will eventually lead to better results.

The next part of the checklist will determine if the strategy will actually make money or not. For example, I could come up with a “strategy” that buys all stocks that start with the letter A, every January, with 100% of my account value, and then sell them in December and repeat with the letter B next January. That fits all the criteria to make it a “strategy”, but now we need to address whether or not it will make money. And last time I checked that is the point of investing, right. We need to be able to answer ‘yes’ to these questions:

- My investment strategy is based on a market truth of how the market really works (ex. momentum, short-term mean-reversion, trend-following, etc. Not “buy in May and go away”.)

- My investment strategy has a repeatable edge that is not sensitive to input metrics, as determined by robust back-testing results (okay, that was the nerdiest thing I wrote today, but it’s very important. Many back-tested systems work because someone tried 487 combination of inputs until they finally got 1 that showed it would generate $200 million in 5 years. If you roll the dice long enough, you’ll eventually roll a pair of snake-eyes 10 times in a row. But we want positive results that work under all market conditions. That’s what I mean by being robust, and not chance.)

- I can calculate the expected return, maximum equity drawdown, and probability of a positive and negative year (again, the only way to know this is because you can back-test a set of rules that you created in step 1 above)

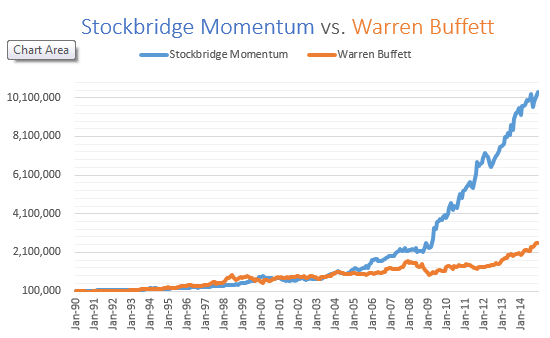

- Finally, once you know the risk and return metrics, does the strategy fit your goals? Does it fit your comfort level? The reason Kahnemann won the Noble Prize in economics for doing research on behavior, is because he knew that at the end of the day, it is investor behavior that has the biggest outcome on our final wealth result, not investment performance. Do you buy at market peaks and sell at market bottoms? Do you exit because you’re currently down 6% even though historically the strategy has been down 10%? Those decisions will have a much larger impact on our final wealth result than anything else in the checklist. Since 1980, even Warren Buffett has had 4 times of losses worse than 30%, and 2 of those losses were worse than 50%! On the upside, he’s outpaced the stock market (that’s investment performance). But how many people can sit through 30% drops, or 50% drops, especially in retirement? That gets to the core of investor behavior. See what I mean?

If you have a portfolio of actively managed mutual funds with internal costs of 1% per year, plus a 1% management fee that’s re-balanced quarterly (like they do at companies that rhyme with “you, “es”, pank”) you have a strategy, it’s just not a very good one, unless you actually like paying high fees and can sit through 50% losses every 8 years. Or, if you buy Disney stock because Star Wars is coming out next week, I’m sorry fellow nerdy friend, but that’s more gambling than investing. Spend your money going to the movie instead! You could even ask a girl to go with you!

Final point: having a pragmatic set of rules to follow for making investment decisions, that will get you closer to your unique financial goals, is where we should focus our time. And in the final analysis, that’s all that really matters. If you want to know “whaddya think of XYZ stock?” call Jim Cramer instead of me. At least he’s entertaining.

Eric Ludwig is a certified financial planner in Madison, WI primarily for a select group of successful professionals and business owners, who among other things aspire to a work-optional lifestyle. Stockbridge has developed and refined a process to put all the pieces of that puzzle together and we call it the Stockbridge GPS process. GPS stands for Goals, Planning, Strategy.